Key markets at a glance:

1 September to 30 September 2024

The Federal Reserve commenced its interest rate cutting cycle with a pre-emptive 0.5% move after declaring its war on inflation over, whilst the real wars in Europe and the Middle East rage on. Escalating tensions between Israel and Hezbollah ensured that gold remained attractive not just for its aesthetics but its status as a ‘safe haven’ for investors. Whilst the precious metal continued to surpass record highs, oil reached a three-year low with Brent crude dropping below $70 highlighting the extent of the divergence in performance.

The US presidential debate left us no closer to gauging the outcome of November’s election, with polls suggesting just a 0.2% differential in Pennsylvania, which looks set to be the key swing state. This uncertainty continues to add to equity and bond market volatility, which started September elevated before subsiding in the latter stages. However, the world’s second largest market picked up the slack, with a stimulus package that saw China in the spotlight for the right reasons, registering its largest weekly gain since 2008. The package equates to 3% of Gross Domestic Product (GDP) and includes cutting mortgage rates on existing homes, loosening reserve requirements on banks to free up capacity for lending and an announcement of stock market reforms. This is no doubt a step in the right direction, but it is likely that a fiscal package will be required to unearth consumer confidence from the doldrums where it currently lies.

Here in the UK, economic data weakened at the margin, but the Organization for Economic Co-operation and Development (OECD) upgraded growth forecasts with the overarching trend a positive one. The Labour government’s rhetoric ahead of the October budget is providing a negative overhang which has temporarily dampened consumer confidence. Nevertheless, the trajectory of the data is upwards and the attractive valuations remain evidenced by record levels of mergers and acquisition activity within the FTSE 350.

On the continent, the recovery continues to be stalled by the contraction in manufacturing, resulting from the excess supply spilling over from China and the consequent price undercutting of domestic companies. This is particularly stark in the auto sector, where big brands including Mercedes-Benz and Stellantis are struggling to compete with their Chinese counterparts and Volkswagen has now profit-warned three times in three months. Meanwhile, inflation has now dropped below the 2% target and given the weakness in the economy, we would expect the Europe Central Bank to ramp up the pace of interest rate cuts.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom

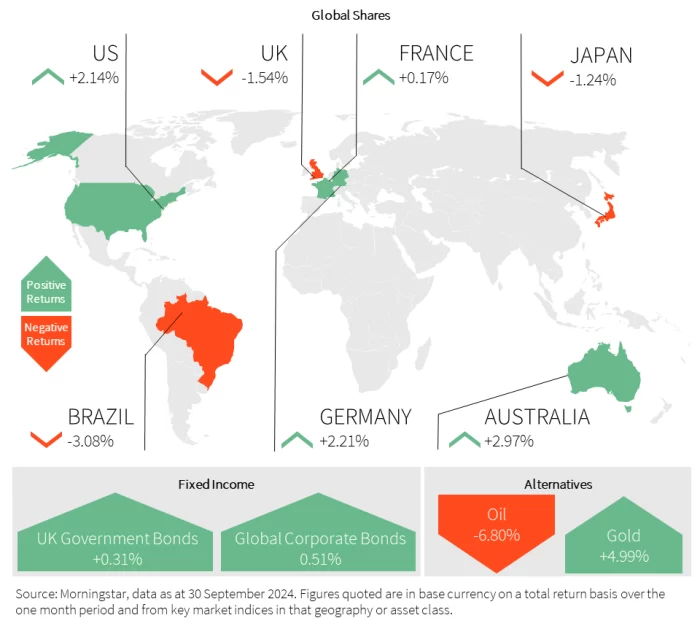

September was a mixed month for UK equities with the FTSE 100 falling 1.54% and the more domestic focused FTSE 250 near flat for the month. The larger cap index was hindered by a strengthening sterling hitting some of the larger dollar-earning constituents. Saudi Arabia reportedly starting to raise oil output to win back market share sent the larger-weighted oil constituents firmly lower. Weaker drug trial results from the largest FTSE constituent AstraZeneca sent their shares down over 10% for the month.

The UK Purchasing Manufacturers Index (PMI), which measures business activity in the services and manufacturing sector, remains firmly in expansion territory, albeit we saw a slight deceleration of growth in the flash September estimates as companies put on hold investment plans ahead of the budget. Economic output grew by 0.5% in the second quarter, slightly less than first thought but remains on track for robust growth this year. The OECD upgraded growth forecasts from the 0.4% predicted in May to 1.1% for this year.

UK inflation remained unchanged at 2.2% in August, roughly aligning with economists’ forecasts. Services Inflation (a key measure of domestic price pressures) rose to 5.6% driven by a substantial increase in airfares, which rose 22% between July and August. Encouragingly, towards the end of the period we saw shop price deflation drop to 0.6% in September with prices falling at their fastest pace since 2021. As expected, interest rates were held at 5%, but it is still expected that the UK sees one more rate cut before the year is out.

In more positive news, mortgage approvals hit a two-year high in August, and according to Nationwide, house prices have risen at their fastest annual rate since 2022. We are, however, seeing signs of consumer and business confidence being hit in the short term. Negative rhetoric on the state of the UK finances, debt-to-GDP hitting 100% and the upcoming October budget have created nervousness.

United States

In September, while the US wasn’t the top performer globally, it outperformed among developed markets. The S&P 500 gained 2.14% and the NASDAQ 100 increased by 2.57%. This momentum was largely driven by the Federal Reserve’s (Fed) 0.5% interest rate cut and Fed Chair Powell’s reassurances about the economy’s strength, which alleviated fears of an imminent downturn. This was the first demonstration of a shift in focus from the inflation mandate to full employment and investors will continue watching labour market data in the weeks and months to come.

Economic data further supports the narrative of a soft landing, with Q3 GDP expected to grow robustly, not far from Q2’s upwardly revised 3% annualised rate. US PMI edged slightly lower, but still exceeded expectations, with services growth offsetting a contraction in manufacturing.

Consumer strength remains mixed but largely healthy. While the Conference Board’s consumer confidence index dropped sharply, the University of Michigan consumer sentiment and retail sales beat forecasts. Positive revisions to Gross Domestic Income (GDI) indicated stronger-than-expected household balance sheets, highlighted by an upwardly revised savings rate.

Housing data also showed tentative signs of stabilisation, with falling mortgage rates spurring refinancing activity, although new buyers remained hesitant, and building permits were revised lower. Meanwhile, inflation continues to moderate, with the core Personal Consumption Expenditures price index rising just 0.10% on a monthly basis, supporting the case for further rate cuts.

With policymakers anticipating 1% of easing by year-end, financial conditions are expected to improve, providing further support for consumers and corporations. Overall, the U.S. economy remains resilient, with a favourable outlook for sustained growth benefiting risk assets.

Europe

September has been a relatively muted month in Europe as the CAC remained flat and the Dax was up just over 2%.

The French government’s hardship endures as Macron’s approval ratings continues to fall, with the economy’s fiscal position an area of concern. France is now running a fiscal deficit over 5% of GDP and is subject to deficit procedures by the EU, which will be difficult to implement with a polarised government.

European Purchasing Manufacturers Index data was uninspiring due to softness in France and Germany. Economies in the south of Europe seem to be performing much better, however it still looks as if growth for the EU as a whole will remain close to 1%. Given the Fed’s 0.5% rate cut, the euro is testing $1.12 and there is little sign of an EU fiscal push, it is likely that Lagarde will take a more dovish stance next month. Following a previously dismissive tone, there will likely be much more openness to an October cut.

The struggle continues in Germany as the ZEW indicator of economic sentiment decreased sharply. Previous hopes of an integrated capital markets union look to be fading as the Berlin government attempts to prevent the takeover of Commerzbank by Unicredit of Italy. This nationalistic agenda limits the likelihood of the Draghi plan being executed, which called for the EU to come together in an attempt to compete with other larger economies such as the US.

Asia and Emerging Markets

The Fed’s recent rate cuts mark a pivotal moment for this region, providing room for local rate cuts and greater fiscal flexibility by easing pressure on currencies.

The most significant news came out of China late in September when they announced their largest stimulus package since Covid-19 in an attempt to shore up the property market and encourage consumers to spend. The announcement followed a slew of weak economic data which left market sentiment at rock bottom. Hence, the reprieve was welcome and both Hong Kong and Shanghai were up over 15% on the month. This rally was largely responsible for emerging markets as a whole rising 8.5%. It remains to be seen whether China will also enact some fiscal easing which we believe is needed for this improvement to become sustained.

Japan, on the other hand, ended the month down with the Nikkei 225 falling 1.4% amid a repricing of interest rate rises. The Bank of Japan held rates steady, accompanied by dovish comments suggesting no urgency for further increases. Nevertheless, the election of former defence minister and monetary hawk, Shigeru Ishiba, triggered a strong rally in the yen. Japan’s headline and core Consumer Price Index met expectations, with a modest rise in inflation expectations. As the virtuous cycle from income to spending gradually intensifies, Japan’s economy is likely to keep growing at a pace above its potential growth rate, with small firms playing a crucial role in driving real domestic demand and sustaining this cycle.

Fixed Income

Short duration high quality corporate bonds provided the strongest performance in the UK in September, as limited exposure to interest rate and credit risk continues to offer the best risk-adjusted returns amidst market jitters and below peak yields. The yield curve flattened with the UK two and 10-year sitting close to 4%. Yields remain more elevated largely due to the stickiness of wage growth, not helped by 7% of the labour force currently claiming long term sick. However, there is some room for increased rate cut expectations after a series of below consensus GDP figures.

Yields continued to fall in the US over the course of the month, with the fall in the short end outpacing that of the long end to normalise the yield curve for the first time in over two years. The market is still pricing in over 2% of cuts to the end of next year, which is likely to only be satisfied in the case of recession, which is not our base case given the continued strong growth and cooling rather than collapsing labour market. This is further supported by Chair Powell stressing that the 0.5% cut was not the new pace and we are more likely to see smaller adjustments going forward.

Elsewhere, the yen has continued to make gains against the dollar and with the market only pricing the next interest rate rise in Japan by October next year, we see more potential upside here. There is clear evidence that wage inflation is now entrenched and as a result, we believe we are likely to see another interest rate rise before then.

Alternatives

Gold’s prolific rally has continued in September, reaching a new milestone of £2,000 ($2,621) per ounce. The combination of the Fed’s 0.5% bumper cut, the dollar hitting a one-year low and the escalation of the conflict in the Middle East have all been conducive to a rising gold price. With Israel now suggesting a possible invasion of Lebanon this geopolitical risk is unlikely to dissipate any time soon. With less than five weeks until the US election, Uncle Sam remains deeply polarised. The uncertainty around the election and the implications of the upcoming vote will likely support the gold price over the coming weeks. Silver has also enjoyed a decent rally towards the end of the month albeit still far from its highs seen during the spring rally. Fears of recession are capping its price, but alternative metals should continue to benefit from gold’s rally. The next few weeks should be supportive for the gold price and the outlook remains positive for further gains. At the current pace, it may not be long until we see the $3,000 milestone breached.

Oil prices fell for the third month in a row as strong supply outlook and questions surrounding demand outweighed geopolitical tensions. Saudi Arabia has now given up on their unofficial target of $100 a barrel of oil as well as indicating a renewed intent to increase supply. With strong production continuing in the US, Canada, Guyana and Iran there would be a large amount of downward pressure on the oil price should Saudi bring the excess supply online. Brent crude had a muted response to the announcement of stimulus in China as traders continue to doubt whether these measures will be enough to boost the weaker than expected demand this year. Unlike gold, the negative news surrounding both the demand and supply side has left no geopolitical premium in the price. Should the US become more involved in the Middle East, this would likely change.

Property

The Nationwide House Price Index in the UK rose by 3.2% year on year this month, marking an acceleration from the 2.4% increase in August. This is now the seventh consecutive period of rising house prices with average prices now sitting just 2% below their record highs seen in summer 2022. The Chief Economist at Nationwide has highlighted that the rapid growth of income has outpaced house price growth. This, alongside reduced borrowing costs, has led to improved affordability for prospective buyers supporting a modest rise in activity and house prices, albeit remaining below historical norms. Net borrowing of mortgage debt by individuals in the UK increased to its highest level since November 2022, whilst the annual growth rate for net mortgage lending rose for the sixth consecutive month. Construction PMI dropped slightly, but alongside consumer confidence this is likely a temporary blip ahead of the October budget.

Important Information

All Index data figures are sourced by Morningstar and correct as at 30 September 2024, unless otherwise stated.